Members of Congress can legally bet on political outcomes, economic crises, and policy decisions using prediction markets — and they face no requirement to disclose those trades. NPR News reported that House and Senate ethics committees have issued no financial disclosure guidance on event contracts or prediction markets, unlike the mandatory reporting rules that govern stock, cryptocurrency, and bond trades.

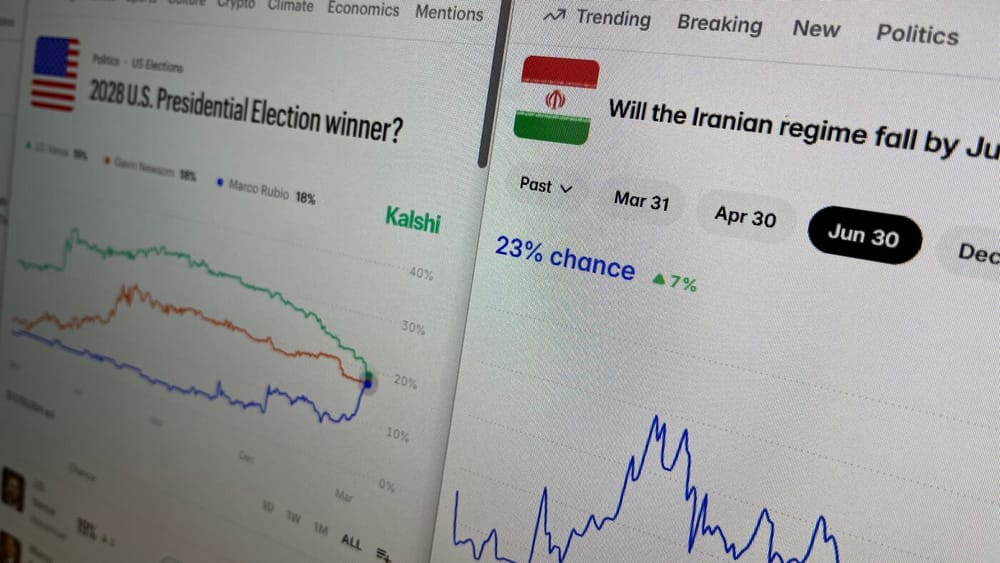

The regulatory vacuum arrives as prediction markets experience explosive growth. Platforms like Kalshi and Polymarket now offer contracts on everything from Federal Reserve interest rate decisions to the timing of military strikes. Lawmakers with access to classified briefings, advance notice of legislative votes, and private conversations with agency heads could theoretically place bets on outcomes they have privileged information about — and the public would never know.

Congressional stock trading has faced mounting scrutiny after multiple investigations documented members buying and selling shares based on non-public information obtained through their official duties. The STOCK Act of 2012 required disclosure of securities trades within 45 days, but prediction markets did not exist in their current form when that law passed. The Commodity Futures Trading Commission classifies event contracts as derivatives, yet they fall outside the disclosure framework that applies to traditional financial instruments.

According to NPR News, some lawmakers have already begun trading on these platforms. The ethics committees' silence on disclosure requirements means the public has no way to track whether members of Congress are profiting from their official positions through prediction market bets. A senator could wager thousands of dollars on the outcome of a bill they are actively negotiating. A House member could bet on the timing of a government shutdown while participating in budget talks. None of it would appear on a financial disclosure form.

The problem extends beyond individual trades. Prediction markets are designed to aggregate information and reveal what informed participants believe will happen. When lawmakers with inside knowledge participate, they distort the market's accuracy while potentially enriching themselves. A well-placed bet by a member of the Intelligence Committee could move the odds on a geopolitical event, creating the appearance of credible intelligence when it is actually self-dealing.

This is not a hypothetical concern. War betting markets have already turned conflicts in Gaza and Iran into speculative instruments, with minimal regulatory oversight. The same platforms that allow users to bet on civilian death tolls and ceasefire timing are accessible to the lawmakers who vote on military funding and receive classified briefings on strike operations.

Ethics reform advocates argue that prediction market trades should face the same disclosure requirements as stock trades, with the same 45-day reporting window and the same penalties for non-compliance. But Congress has shown little interest in restricting its own financial activities. The STOCK Act itself was passed only after a 60 Minutes investigation and sustained public pressure. A decade later, enforcement remains weak and the IRS has lost a quarter of its staff to budget cuts, further eroding accountability mechanisms.

The silence from ethics committees is a choice. They could issue guidance clarifying that prediction market contracts must be disclosed. They could recommend legislative fixes to close the loophole. Instead, they have said nothing, allowing a regulatory gap to widen as the industry grows. The longer the delay, the more entrenched the practice becomes — and the harder it will be to impose transparency requirements on lawmakers who have already profited from the absence of rules.

What makes this particularly corrosive is the asymmetry. Ordinary Americans who trade stocks or cryptocurrency face strict reporting requirements if they work in regulated industries or hold security clearances. Members of Congress, who hold far greater power and access to non-public information, face no such burden when betting on the very outcomes they help determine. The message is clear: the rules are for other people — a pattern that federal ethics exemptions have reinforced across multiple branches of government.